About i360’s Consumer Pulse: The Consumer Pulse asks 1,000, of the 2.5 million US adult panelists, over 150 questions daily. Questions center around key topics such as economy, lifestyle, real estate, automotive, shopping, employment, political opinions, and more.

Is a recession coming our way? The Wall Street Journal recently polled academic and business economists and placed the probability of a recession within the next 12 months at 61%. Three-quarters of the same economists also expressed doubts that the Fed would be able to avoid widespread economic contraction via the ever-elusive “soft landing”. Coupled with economist’s projections, Powell’s barrage of rate hikes seems to point towards an imminent recession within the next year, while other metrics tell a different story.

The U.S. Bureau of Labor and Statistics January 2023 jobs report boasted that over half a million jobs were added in January alone. Additionally, unemployment is at its lowest levels since 1969. For reference, the US hasn’t seen unemployment levels this low since the first moon landing – before the Nixon administration. So, are we really barreling down on another pull-back, or is the old adage still true that economist have predicted nine of the last five recessions?

While expert opinions are undoubtably important, what do consumers think? i360’s Consumer Pulse, a longitudinal survey, has been tracking consumer sentiment on this topic. Below we take a look inside Consumer Pulse to get a better view.

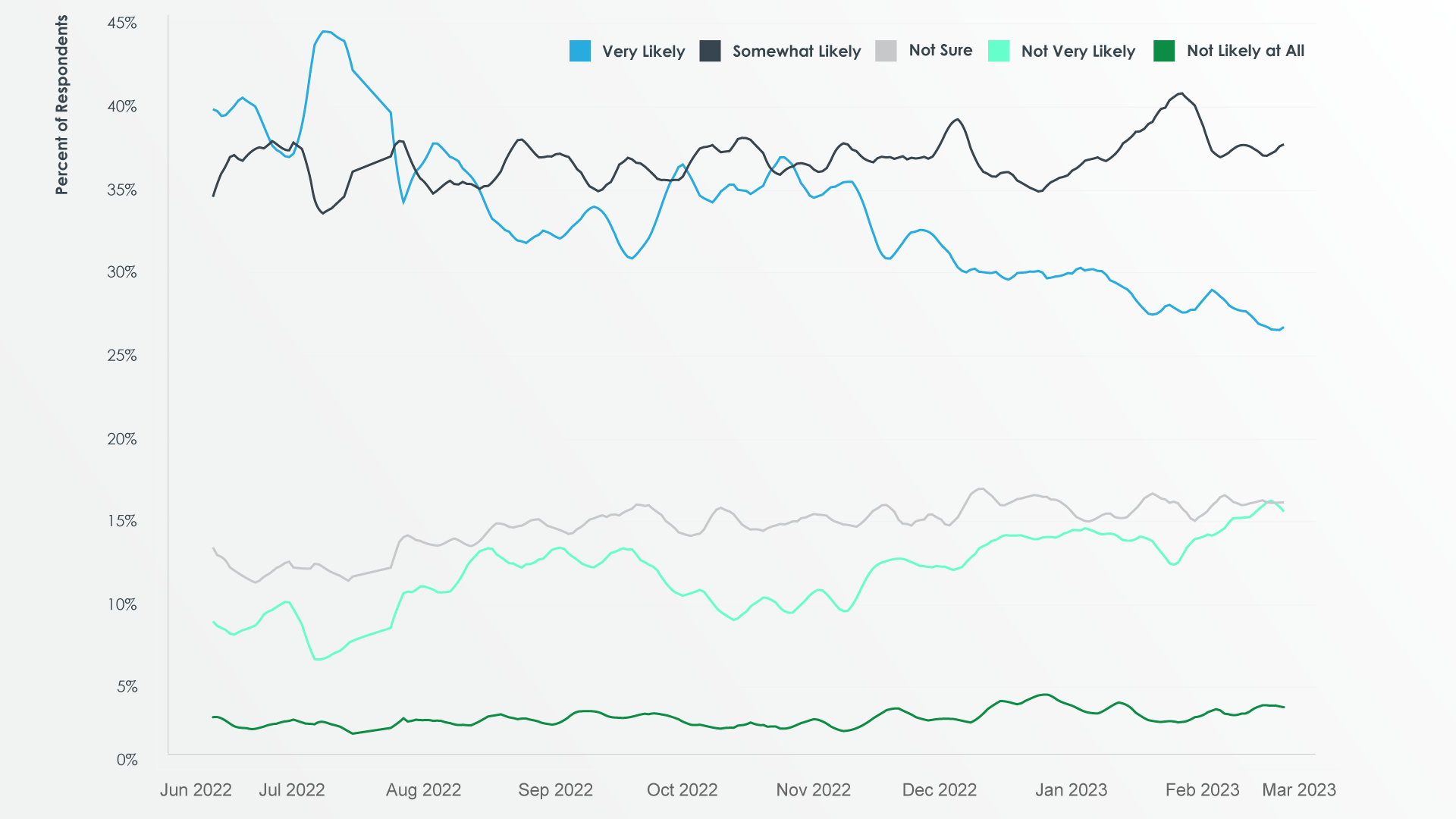

The following chart shows our respondent’s outlook on a possible recession. General sentiment in our data is consistently bearish, with 70-80% of Americans feeling that the US is at least somewhat likely to enter a recession soon. After the Fed raised rates eight times in less than a year, it is reasonable to anticipate that the downstream effects would start to impact recession expectations. However, the most bearish answer of “Very Likely to Enter an Economic Recession”, recedes as the Fed increases rates. All other responses, ranging from “Not likely at all to enter an economic recession” to “Somewhat likely”, remain reasonably stationary across time.

Over the next six months, do you think we are likely or not likely to enter an economic recession?

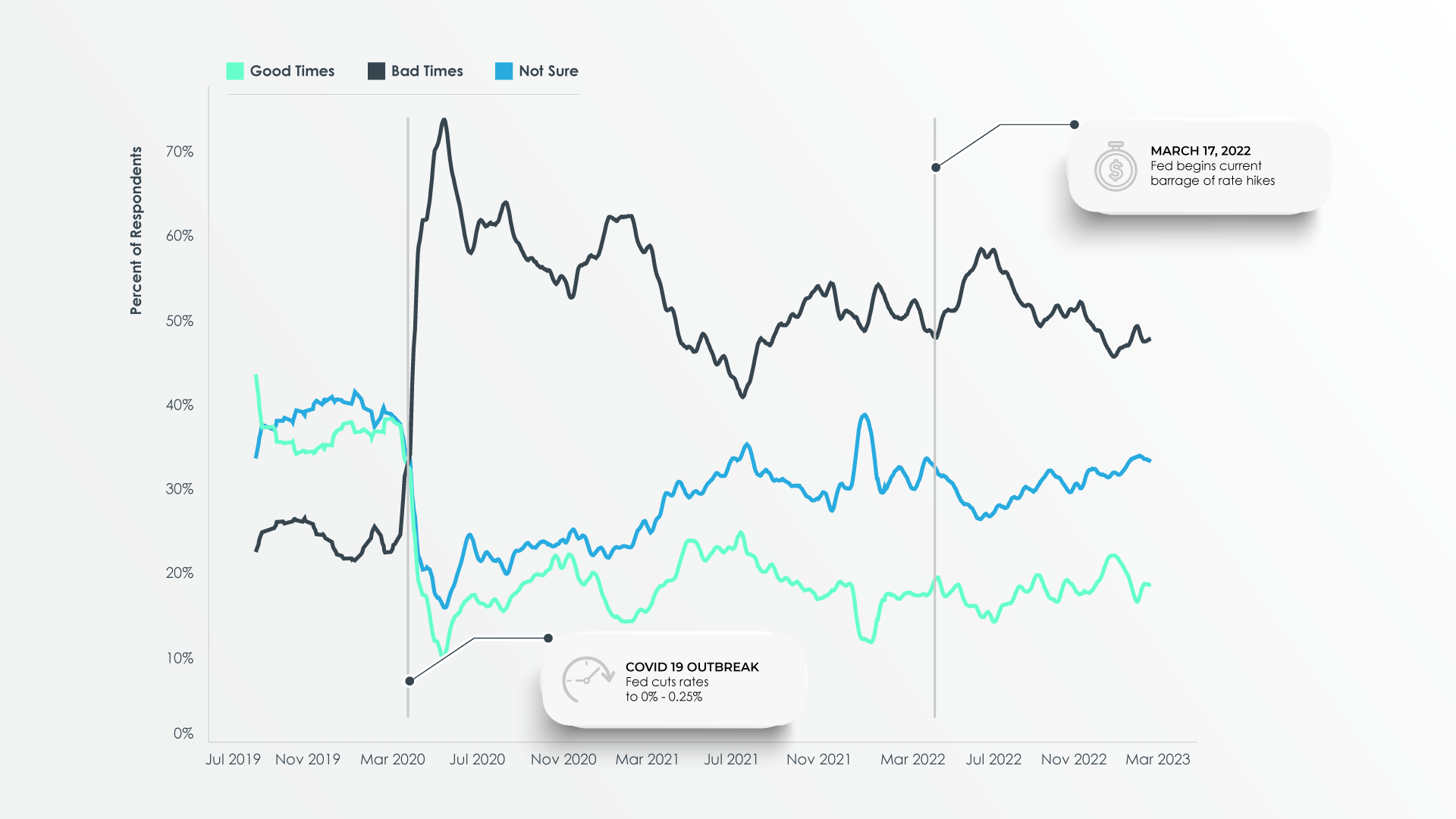

Consumer Pulse also asks respondents to classify current business trends as ‘good times’, ‘bad times’ or ‘unsure’. In contrast to responses on recession likelihood above, survey responses for this question are consistent with the common ‘Fed Hikes Rates’ headline narrative. Beginning with the initial set of rate hikes in March 2022, respondents displayed an increased level of bearishness at an accelerating rate. In July 2022, negative sentiment apexes well above that of Winter 2021 levels, until arriving at the current rate of ~50%. Under a quarter of respondents classify the current business environment as ‘good times’, with one-third being unsure. Sentiment towards rate hikes seems more reactive and indicative of a recession from this perspective, but could point toward consumer short-sightedness concerning Fed policy implications.

How would you rate business conditions in the United States today?

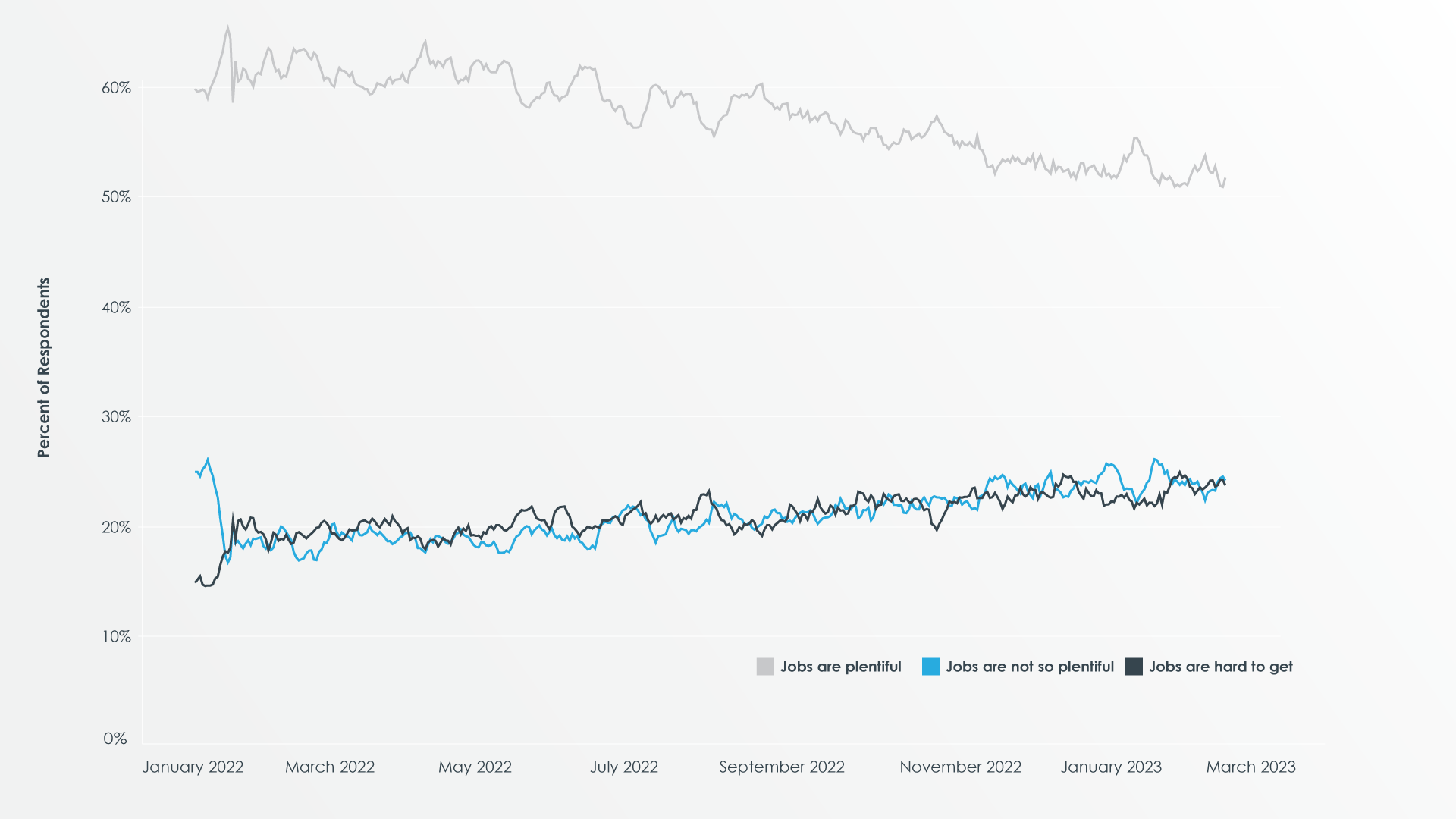

Lastly, what do respondents think about the current job market? Over the course of the last year Consumer Pulse shows the slow erosion of positive labor market sentiment. This pattern continues despite the 500,000 plus jobs added in January. Regardless of incremental changes, most consumers remain positive about their role in the labor market. The reality of strong labor demand isn’t generating kinder sentiments toward the general economy. This is unexpected and will be explored in a future Consumer Pulse analysis.

How would you rate employment conditions in the U.S. today?

Consumer Pulse respondents generally express a negative, but elastic, outlook on the business environment and consistent bearishness towards the general economy. Will the US economy continue to rapidly add jobs? Or will these rate increases catch up and be ‘too much too fast’ for consumers? As Consumer Pulse continues to monitor sentiment, follow along for a wide variety of economic, financial and consumer analysis.

Disclosure: The information in these blog posts, based on i360’s Consumer Pulse, is for informational purposes only and should not be construed as investment advice on any matter.